Debit and credit card processing is not just a necessary operational function for issuers and acquirers; it’s a critical component that directly influences cost efficiency, customer satisfaction, and overall profitability. In an increasingly cashless society, understanding the full spectrum of credit card processing—from the roles of key players to the nuances of fee structures—is essential for players in the card payments ecosystem that want to maintain a competitive edge.

By thoroughly optimizing these elements, institutions can significantly enhance their payment systems, reduce unnecessary costs, and improve customer experiences, positioning themselves as leaders in the financial sector. For leading experts in card payment consulting, like Intelica, this optimization is a cornerstone of our strategic approach.

The Key Players in Card Processing

In any card transaction, several key players are involved, each serving a specific role that influences both the efficiency and the cost of the process. These roles must be clearly understood by financial institutions to optimize their transaction processing systems:

Merchant

The business accepting the payment. This entity is involved in the actual transaction with the customer, typically offering goods or services in exchange for electronic payments.

Cardholder

The customer making the purchase. They use their credit or debit card to complete a transaction.

Acquirer

The financial institution that accepts payments on behalf of the merchant. Acquirers work directly with merchants to facilitate payments and the transfer of money into their bank accounts. An important distinction is that an acquirer can also function as a processor; however, not all acquirers are processors, and vice versa. These are distinct business functions, even though they can sometimes overlap.

Processor

The entity responsible for handling and executing electronic transactions accepted by the acquirer on behalf of the merchant. The processor ensures that payment information is correctly transmitted among the acquirer and card networks.

Card Associations

Entities like Visa and Mastercard that set the rules and fees for transactions, governing how payments are processed across their networks.

Issuer

The institution that issued the credit or debit card to the customer, typically a bank or a credit union.

By clearly defining and understanding these roles, financial institutions can more effectively manage and optimize their debit and credit card processing operations, ensuring that each transaction is handled as efficiently and cost-effectively as possible.

Card Associations

Entities like Visa and Mastercard that set the rules and fees for transactions, governing how payments are processed across their networks.

Issuer

The institution that issued the credit or debit card to the customer, typically a bank or a credit union.

By clearly defining and understanding these roles, financial institutions can more effectively manage and optimize their debit and credit card processing operations, ensuring that each transaction is handled as efficiently and cost-effectively as possible.

The Payment Process: An Overview

Credit card transactions involve a series of steps that each have implications for both cost and security. Financial institutions must have a deep understanding of these processes to manage them effectively:

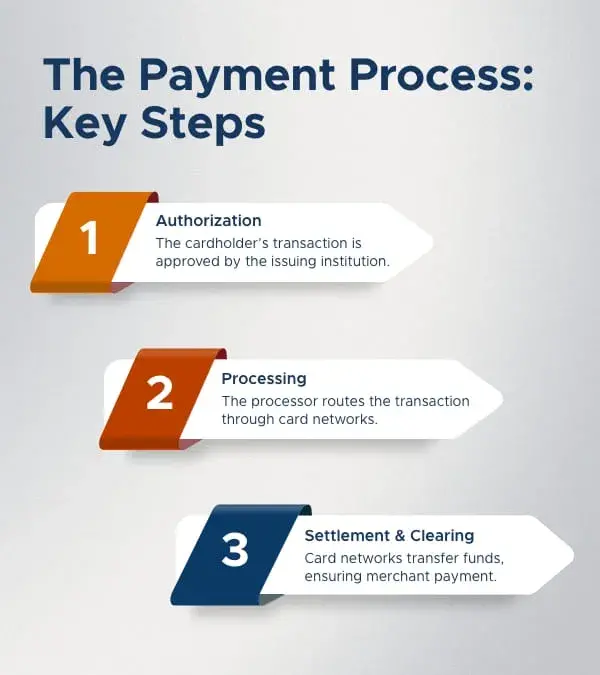

Authorization

The cardholder initiates a transaction, which is authorized by the issuing institution.

Processing

The transaction is routed through the payment processor, often involving card networks like Visa or Mastercard, to the acquiring institution.

Settlement and Clearing

Card networks such as Visa and Mastercard play a key role in the settlement and clearing process. They facilitate the movement of funds between the issuing and acquiring institutions, ensuring that the payment is transferred to the merchant's account after deducting the relevant fees.

Understanding this flow, including the role of card networks, is critical for financial institutions to manage and optimize their credit card processing systems effectively. For more details on how this works, you can explore our Interchange Analytics service.

Fee Structures & Pricing Models

The fees associated with card processing can be complex, and the pricing model chosen by an acquiring institution can have a significant impact on its profitability. Here are the most common pricing models used in the industry:

Interchange-Plus Pricing

Offers transparency by separating the interchange fees from the processor’s markup, but it can result in fluctuating costs depending on the volume and type of transactions. Additionally, the IC++ model further breaks down transaction costs by separating interchange fees and associated fees, providing even greater clarity and control over transaction expenses.

Flat Rate Pricing

Simplifies budgeting by offering a consistent rate, but it may not be the most cost-effective option for high-volume acquirers.

Tiered Pricing

Categorizes transactions into different tiers with varying rates, which can obscure the true costs and potentially increase overall expenses.

Selecting the right pricing model is essential for optimizing financial performance. Our Interchange Analytics service is designed to help financial institutions navigate these complexities. We provide in-depth analyses and actionable insights that enable our clients to optimize their interchange fee structures and pricing models, ensuring maximum profitability and cost efficiency.

Enhancing Operational Efficiency with Technology

Leveraging advanced technology is essential for financial institutions seeking to improve the efficiency and security of their card processing operations. The right technology not only streamlines processes but also provides valuable data insights that can lead to better decision-making.

Our proprietary platform, incontrol, plays a critical role in enabling data monitoring and analytics specifically related to payment processes. With incontrol, institutions can view information related to all key players in a single platform and quickly identify and address issues. Additionally, incontrol offers specialized dashboards for interchange, allowing institutions to monitor interchange rates, analyze trends, and optimize strategies to improve profitability. It also provides insights into transaction-related fee costs, enabling more precise financial management.

Driving Success with Optimized Payment Processing

Mastering the complexities of credit card processing is about more than just ensuring transactions are handled efficiently—it’s about creating a strategic advantage that drives profitability and enhances customer satisfaction. By focusing on key elements such as fee structures, technology integration, and compliance, institutions can optimize their processes, reduce costs, and offer superior services.

At Intelica Consulting, we are committed to helping financial institutions navigate these challenges with tailored solutions that meet their specific needs. Learn more about our leadership team and history, and don’t hesitate to contact us for personalized assistance with your payment processing needs.